As you know, the balances in asset accounts are increased with a debit entry. They are helpful when reconciling accounts to print statements, clearing errors, etc. They can also be helpful when reconciling accounts for pulling reports.Another example would be where you deposit cash, but the teller doesn’t post it correctly. You have to go back and compare your records with the bank’s to try and figure out what went wrong so you can correct your records to match the banks. By comparing the two statements, Greg sees that there are $11,500 in checks for four orders of lawnmowers purchased near the end of the month. These checks are in transit, so they haven’t yet been deposited into the company’s bank account.

Step 1 of 3

For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation. Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications. Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others.

- To reconcile your bank statement with your cash book, you’ll need to ensure that the cash book is complete and make sure that the current month’s bank statement has also been obtained.

- Nowadays, all deposits and withdrawals undertaken by a customer are recorded by both the bank and the customer.

- For example, you wrote a check for $32, but you recorded it as $23 in your accounting software.

Step 3: Adjust the bank statements

Once the underlying cause of the difference between the cash book balance and the passbook balance is determined, you can then make the necessary corrections in your books to ensure accuracy. Today, online banking and accounting software offer real-time feeds and automated transaction matching. As a result, bank transactions can be automatically imported into an accounting software, where one is able to categorize and match a large number of transactions with one click of a button. This significantly reduces the effort that goes into the reconciliation process and enables businesses to verify their cash balances anytime throughout the month.

How Often Should You Reconcile Your Bank Account?

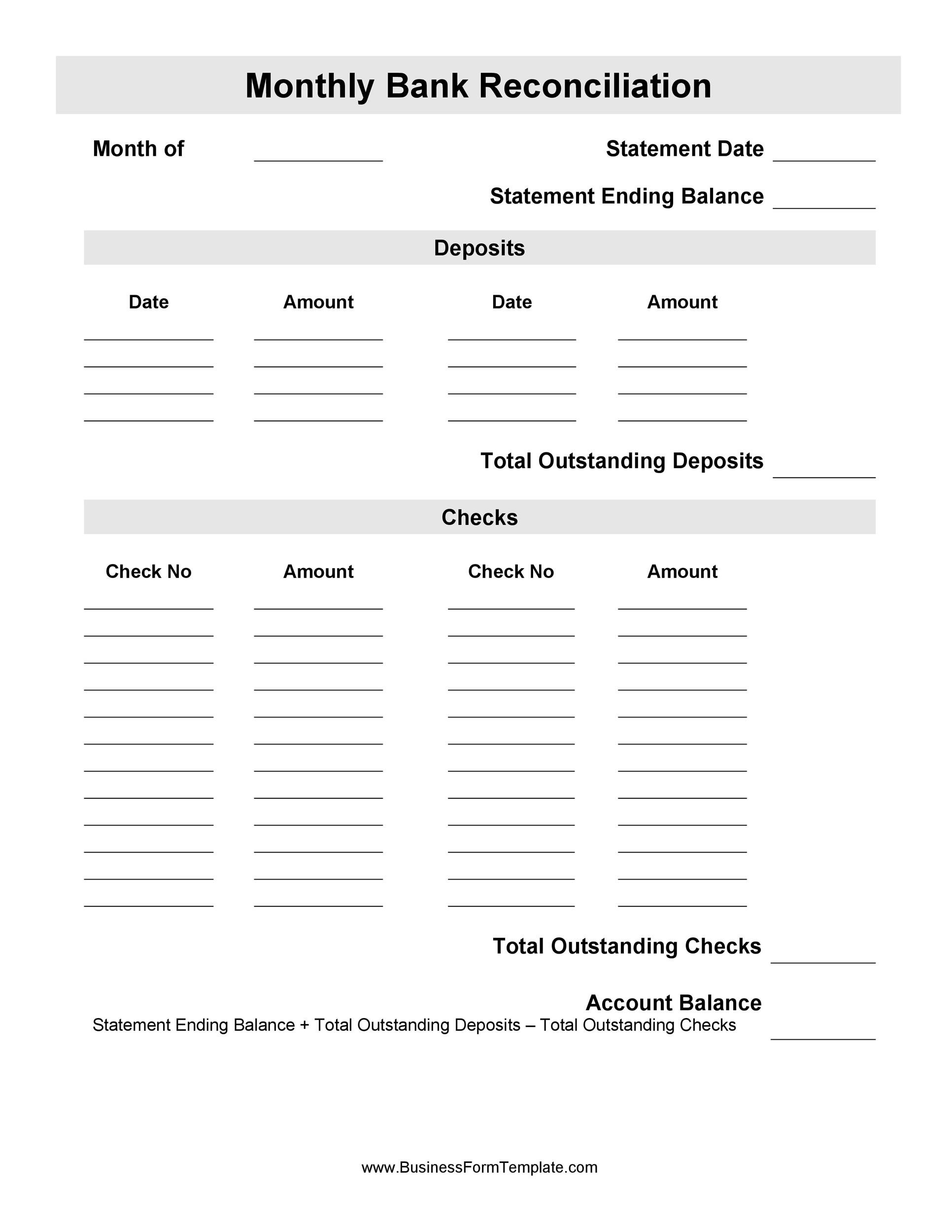

This is due to the time delay that occurs between the depositing of cash or a check and the crediting of it into your account. When your business issues a cheque to suppliers or creditors, these amounts are immediately recorded on the credit side of your cash book. However, there might be a situation where the receiving entity may not present the cheques issued by your business to the bank for immediate payment. This is due to the time delay that occurs between the depositing of cash or a cheque and the crediting of it into your account. Deduct from the bank statement balance the proceeds of any check that you have issued and entered in your accounting record but have not been presented to paid by the bank. Add to the bank statement balance all deposits that are shown by your accounting record but have not been entered in the bank statement.

There could be transactions unaccounted for in your personal financial records because of a bank adjustment. This may occur if you were subject to any fees, like a voucher ideas examples 2023 monthly maintenance fee or overdraft fee. For interest-bearing accounts, a bank adjustment could be the amount of interest you earned over the statement period.

Step 1: Collect the business and bank records

All transactions between depositor and bank are entered by both the parties in their records. These records may disagree due to various reasons and show different balances. The purpose of preparing a bank reconciliation statement is to find and understand the reasons of this difference in account balance.

When your business receives cheques from its customers, these amounts are recorded immediately on the debit side of the cash book so the balance as per the cash book increases. However, there may be a situation where the bank credits your business account only when the cheques are actually realised. Find all checks that you have issued but have not been presented for payment. You can do so by comparing the checks issued in your accounting record with the checks honored as per your bank statement. If your accounting record shows that a check has been issued and your bank statement does not show a corresponding entry for that check, it means that it is an outstanding or unpresented check.

Since you’ve already adjusted the balances to account for common discrepancies, the numbers should be the same. Next, check to see if all of the deposits listed in your records are present on your bank statement. Whatever method you prefer, it’s important to keep solid records of every transaction to reconcile your bank account properly. Ideally, you should run a reconciliation each time you receive the statement from your bank.

Or there may be a delay when transferring money from one account to another. Or you could have written a NSF check (not sufficient funds) and recorded the amount normally in your books, without realizing there wasn’t insufficient balance and the check bounced. Bank reconciliation statements are effective tools for detecting fraud, theft, and loss. For example, if a check is altered, the payment made for that check will be larger than you anticipate.

Infrequent reconciliations make it difficult to address problems with fraud or errors when they first arise, as the needed information may not be readily available. Also, when transactions aren’t recorded promptly and bank fees and charges are applied, it can cause mismatches in the company’s accounting records. A bank reconciliation statement can help you identify differences between your company’s bank and book balances. A bank reconciliation compares a company’s cash accounting statements against the cash it has in the bank. A bank reconciliation is used to detect any errors, catch discrepancies between the two, and provide an accurate picture of the company’s cash position that accounts for funds in transit. How you choose to perform a bank reconciliation depends on how you track your money.